As the Chinese Lunar New Year draws to an end, the container lines have already prepared themselves for a strong rebound. In fact they must have been expecting volumes to go up in the short term, as most liner companies have hesitated to pull capacity out of the market during the past three months' slowdown.

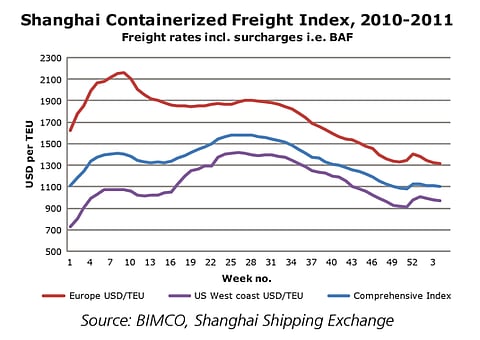

During 2010 the main container lanes experienced very healthy growth rates but at an uneven pace. The main trading lane from Asia to Europe was quick to improve and showed strong volumes. Meanwhile, US consumers were comparatively hesitant but came back with a vengeance during the second and third quarter. Freight rates were following similar trends, with spot rates from Shanghai to Europe peaking in early March and rates to the US West Coast peaking early July.

As the year came to a close, volumes contracted and so did freight rates. In early November BIMCO estimated that more than 300 vessels had to be temporarily withdrawn from service to balance supply and demand and to prevent freight rates from falling further. This did not happen, as only 140 vessels were idled. Rates have dropped 10-11 percent since then.

Despite a small positive hiccup in freight rates around year-end, rates have continued to slide for more than half a year. With bunker prices increasing by US$100 per tonne since October, and failing the implementation of the announced General Rate Increases during January, BIMCO estimates that only the most cost-efficient liner companies are making money on the Far East to Europe trade at current rates – US$1,316 per TEU.

For the trans-Pacific trade lanes it is worthwhile to notice that even though volumes grew by 18 percent in 2010 as compared to 2009, 2010 volumes are still 12 percent lower than the peak year of 2007. US demand is expected to remain weak, although there are indications of enhanced consumer confidence. Recovery is fragile and we might still see another year of sub-2007 volumes since US consumers are buying fewer Asian goods. The good thing, however, is that most economists are discarding the feared double-dip.

According to Clarkson's, the 800,000TEU of very large Post-Panamax ships (6,000+TEU) that entered the fleet during 2010, did not materially impact the main lanes, as the extra capacity was cascaded onto north-south and intraregional trade lanes.

Supply:

Thirty-one Ultra Large Container Ships (ULCS) with a cargo capacity of more than 10,000TEU came on stream during 2010. These ships entered almost exclusively onto Far East – Europe services. This was a shortfall of 50 percent in comparison with scheduled deliveries and a bit more than the overall slippage of some 40 percent. During January 2011, four ULCSs have already been delivered, and 54 additional ULCSs are scheduled for delivery in 2011. Even with another year of substantial slippage in deliveries this will be massive and make more cascading happen. Slow and super-slow steaming will stay – there is no way around it – in order to maintain sustainable utilisation levels across the fleet.

On average, newbuilt vessels will be about the same size as 2010-deliveries. But the large amount of newbuild ULCSs set to be launched during the first half of 2011 will be one to watch out for. In 2010, 25 of the 31 megaships were delivered later than scheduled and during the second half – a clear evidence of the serious postponement efforts by owners. As oversupply is a true risk and the biggest single challenge to the container trades, later than expected arrivals of fewer than scheduled ULCSs would be a welcome outcome.

The active fleet has grown by 0.7 percent so far in 2011, caused by deliveries of 92,525TEU in the form of 15 newbuild vessels, with no vessels being demolished.

BIMCO forecasts an inflow of new container tonnage in 2011 to be less than in 2010 at 1.2 million TEU. As demolition is expected to be insignificant the fleet is forecasted to grow by 8.3 percent in 2011.

In 2010, vessels in the larger post-Panamax segment, sized between 7,500 and 10,000TEU, represented the greatest demand with yards. All of these vessels are expected to be delivered in 2013-2014 and therefore pose no immediate additional challenges to the relevant markets.

Outlook:

Present freight rate levels are not expected to improve during the first quarter of 2011 and may prove to be sticky going into second quarter if the fundamental supply-demand imbalance remains a drag on freight rates. Too much tonnage is suppressing utilisation levels down to 80 percent, leaving little room for upside risk. However, downside risks still remain very real even though inflow of new tonnage is close to getting matched by demand growth.

In the light of the firmness of average freight rates in 2010 that took many by surprise, freight rates are likely generally to stay lower in 2011. The strong market on Asia-Europe during the first quarter of 2010 is very unlikely to happen again. In combination with a second year of high capacity inflow of tonnage suitable for Asia-Europe, that trade and the ones affected by eventual cascading, will feel most of the heat. Certain sub-segments and trades are likely to be squeezed as cascading takes its toll.

Meanwhile, containerised imports to US from Asia are in for a more positive year – rates may hold up better than Asia-Europe freight rates, but still go down. Overall, BIMCO expects Asia-US freight rates to be more stable due to the contract structure of the trans-Pacific trade as well as an expectation that US imports volume-wise should go up as the US economy gets into more sustainable territory.

Bunkers remain a crucial cost element in particular for containerships, and since the beginning of October, bunker prices have increased by 22.5 percent from US$450 per tonne for 380 CST in Singapore, to US$550 per tonne by the end of January. This made liner companies push for an increase in the fuel surcharge known as bunker adjustment factor (BAF). This may be the main reason for the minor positive hiccup in Shanghai spot rates across the board taking place in the early weeks of 2011.

Since the rate stabilisation efforts appear unsuccessful, the focus on slow steaming and resumed idling of vessels remains on top of the agenda as the most effective counters to rising cost levels and a means for carriers to stay profitable.

BIMCO

www.bimco.org