OPINION | Bad crude oil tanker market struggles to find solid support

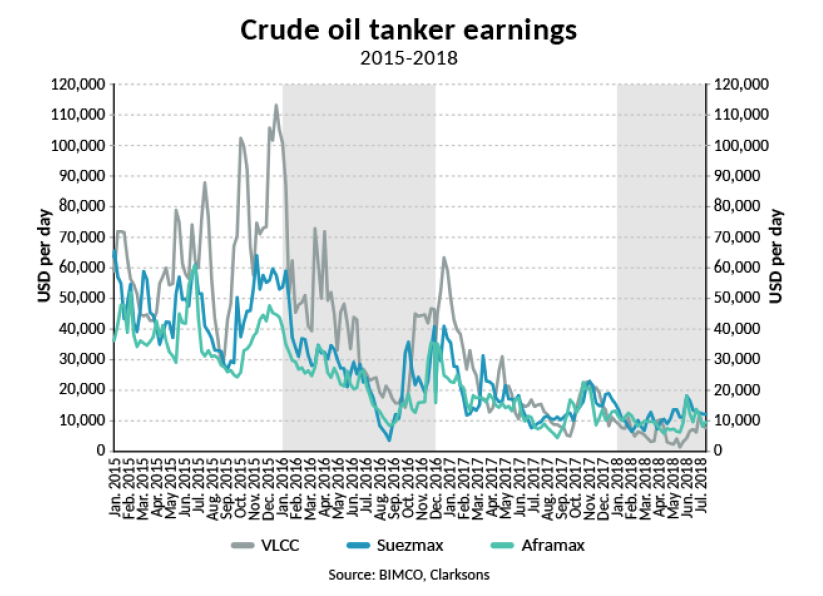

Crude oil tanker earnings have since records began, never been this bad. Earnings for very large crude carriers (VLCCs) in the first half of 2018 were as low at US$6,001 per day on average, with a Suezmax tanker earning US$10,908 per day and an Aframax making US$9,614 per day – All heavily loss-making levels for an industry which needs a much-improved fundamental market balance to lift freight rates above break-even levels into profitable territory.

Having enjoyed a very strong 2015 that saw the highest freight rates for crude oil tankers in seven years, 2016 was a step down, but still profit making. As the crude oil tanker fleet kept growing faster than demand in 2017, loses returned to the industry, after three profitable years.

“2018 has been absolutely horrible for the crude oil tankers with freight rates and the fleet utilisation rate falling to a record low level,” said BIMCO’s chief shipping analyst Peter Sand.

“The total crude oil tanker fleet hasn’t grown at all in 2018. In fact, the VLCC and Aframax fleets specifically haven’t been growing over the past 12 months. The freight market is severally impacted by very weak demand growth.

“Overall, the freight market is oversupplied. The key to higher earnings lies within a very low fleet growth and a return to normalised demand level. The sooner the better – but patience is required.”

A long-winding year

When can we expect crude oil tanker freight rates to deliver profits to owners and operators again? And when will overcapacity be significantly reduced? Most likely we must wait until the second half of 2019 before an improved market balance will yet again deliver profits to the industry.

What could trigger a faster recovery?

Since the beginning of 2018, massive demolition activity of excess capacity in the crude oil tanker sector has resulted in an unchanged fleet size. This is a critical element for a recovery to develop. 13 million DWT was demolished in the first half of 2018. Moreover, a different oil market balance may also cause a return to an oil price contango (contango is a situation where the future price of a commodity is higher than the spot price). An oil price contango is likely to indicate an increased demand for tankers for floating storage.

The fundamentals matter

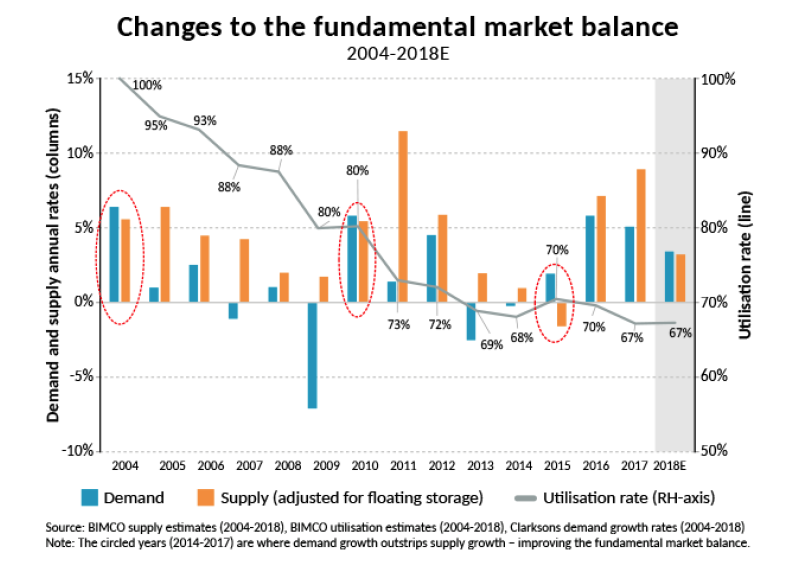

When conducting a fundamental analysis of the crude oil tanker market the focus is on calculating the utilisation rate of the fleet, with the aim of developing a strong correlation between that and the actual freight rates. For the dry bulk market, that correlation is very strong, and we have used it to show the road to recovery for the dry bulk market. For the crude oil tanker market, the correlation is weaker, but still strong enough to rely on for directions – is the market going up or down?

In the short term, freight rates may react more than the underlying tanker market fundamentals indicate. 2018 is an example of that. The first half of the year has seen a very serious deterioration of freight rates when compared to 2017. A drop which the medium to longer term fundamental changes alone cannot explain.

Therefore, changes to the utilisation rates mostly give an indication of the direction of the market, up or down. Much more than a specific freight rate level. For that reason, BIMCO keeps its focus on changes to the supply-demand balance as such, more than forecasting specific freight rate levels for the coming years.

For the supply side, it is important to acknowledge the impact of floating storage. When low, it’s irrelevant, but when it becomes widespread it provides a positive trigger to the market, as the available trading fleet becomes nominally smaller. The correlation between freight rates and utilisation improves quite a lot, when adjusting for floating storage as we do here.

Floating storage affects short term

Taking floating storage into the calculations provides an understanding into the volatility over recent years and particularly the improvement in freight rates seen in 2015. That year saw a significant increase from 2014, where 20 units on average were deployed for floating storage. During 2016 an average of 44 VLCCs were used for storage meaning that the nominal fleet growth, as measured by DWT only, was more than reversed by capacity “taken out of active trading” for floating storage purposes.

In 2016, the amount of floating storage was even higher, but inefficiencies in fleet operations that had also contributed to a reduction in active fleet growth in 2015 had eased – driving supply side growth higher than demand side growth. That resulted in freight rates reducing from 2015 to 2016. 2017 saw a low level of floating storage. This meant that the supply side grew faster than the nominal fleet development. As supply (adjusted for floating storage) significantly exceeded an otherwise solid demand growth, freight rates and fleet utilisation rates dropped.

Floating storage is a key element of the dynamics of the crude oil carrier market due to its impact, when it becomes big enough, and unpredictable nature which reflects the very volatile oil market. It is a dynamic factor that we do not see in other bulk trades.

Asian demand is increasingly dominating the market

The general trend over the past ten years has been one of oil demand and oil imports growing in China and India; and oil imports contracting for the most part in North America. Crude oil tanker shipping has benefitted from longer sailing distances to China, but naturally needs Chinese import volumes to continue to grow even if North American imports are not likely to reduce much further.

The supply side will command the future

110 VLCC is what is left in the order book, and that is the figure that matters. The order book also holds 50 Suezmax and 124 Aframax tankers, but that doesn’t really matter in the bigger picture. The VLCCs are scheduled for delivered within the next 33 months. Naturally, owners are in intense talks with shipyards about possible postponements of delivery dates as the market is bad right now.

“It seems safe to say that the supply side holds the key to an improved freight market – and the change of the utilisation rate provides the direction of the market,” added Peter Sand.

“Keeping crude oil tanker demolition activity high while holding back on contracting new ships is required to tame the fleet growth, today and tomorrow.

“How big a task the supply side is faced with will depend very much on the future demand for floating storage capacity. A big juicy oil price contango in 2019 would have a major positive impact on freight rate levels. It is not possible to predict if a significant contango will materialise and that is why we cannot make a firmer prediction as to when real improvements will appear.

“Demand side growth may ease the way towards healthier freight rates, but its support in the coming years seems uncertain and cannot be relied heavily upon.”

As BIMCO has said before, 2018 is set to become another loss-making year for the crude oil tanker industry. Looking ahead, the year when the industry will return to profitable freight rate levels depends on the supply side growing (adjusted for the use of floating storage) at a much lower level than the demand side. Small improvements to the fundamental balance will not be enough to turn around the market.