FEATURE | New Russian/Iranian sanctions to “suppress potential growth”

New sanctions on Iran and Russia won’t derail the container market recovery, but would suppress potential growth.

US President Donald Trump’s unilateral decision earlier this month to pull his country from the Iran nuclear deal (the Joint Comprehensive Plan of Action that was co-signed by Iran, China, the European Union, France, Germany, Russia and the United Kingdom in July 2015), has the rest of the world scrabbling for a Plan B.

Should negotiations fail to resolve the matter all non-US countries will be faced with a thorny dilemma: how to continue trading with Iran without catching heat from America? The threat of so-called “secondary sanctions”, whereby the US punishes foreign firms for doing business with Iran, will inevitable see companies acquiesce to the demands of the biggest market. MSC, the world’s second largest container line, is reportedly no longer serving Iran.

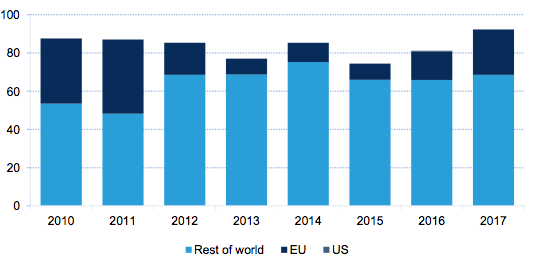

This won’t be such a problem for US companies as America barely does any trade with Iran. Figure 1 shows a breakdown of Iran’s trading partners this decade and the US’ share of two-way trade is virtually imperceptible on the chart at just 0.4 per cent last year. The EU, on the other hand, has rapidly been reacquainting itself with Iran since the end of sanctions in 2016, rebuilding its trade share to 25 per cent last year. It had been around 45 per cent in pre-sanctions 2011.

When economic sanctions were imposed on Iran at the start of 2012 the impact on container trade was instantaneous. Port throughput in the country decreased by 18 per cent that year and by 2015 box handling had shrunk by 36 per cent since 2011.

Russia experienced a similar trough when in September 2014 Western countries imposed financial sanctions for the annexation of Crimea and war in the Ukraine. Russia’s port throughput plummeted by 26 per cent in 2015, although the downturn was shorter-lived than it was for Iran as Russia managed to better adapt to its less imposing restrictions (an upturn in oil prices helped too), seeing container handling rise once again from 2016.

In April this year, due to perceived “malign activities” the US proposed to extend the Russian sanctions to outlaw doing business with a number of individuals and big companies, while the EU is doing similar. These new sanctions on Russia highlight the growing tensions with the West and signal that an end to such measures is a distant possibility at best. Maersk Line and MSC quickly announced they would not accept bookings or payments from any designated person or company on the US Treasury’s sanctions list.

So how big an impact on world container demand will worsening trade conditions for Iran and Russia have?

The answer is surprisingly little considering both countries’ size and importance on the world stage. The recoveries in Iran and Russia only provided a marginal benefit to overall container demand growth last year. Drewry estimates that Iran’s container port handling throughput increased by approximately 580,000 TEU in 2017, while Russia’s improved by a little over 630,000 TEU.

Significant sums in isolation, but combined still only around three per cent of the additional 44 million TEU total port moves made last year. Had either country miraculously tallied exactly the same port handling figure as in 2016, the world growth rate in 2017 would only have dialled back by 0.2 percentage points from the actual annual rate of 6.3 per cent.

The risk presented by more sanctions, therefore, is less about derailing gains already made in the container market; rather it is about quashing potential future growth.

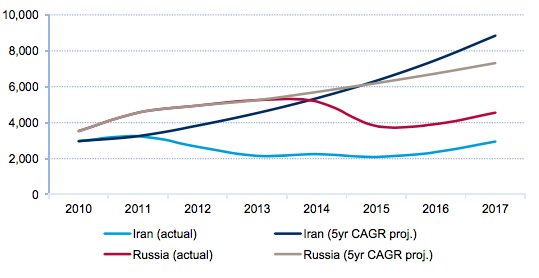

Neither Iran nor Russia has made it back to their pre-sanctions peak container throughput years: Iran’s total of 2.95 million TEU last year is only 91 per cent of its record year in 2011, while Russia’s sum of 4.55 million TEU is only 87 per cent of the 2013 high.

Before sanctions were imposed in 2012 Iran’s container port handling enjoyed stellar five-year CAGR growth of 18 per cent, while in the five years leading to Russia’s more limited sanctions in late 2014 its port throughput CAGR was nearly as impressive at nine per cent. Had both countries not been banished to the naughty step and maintained those annual growth rates they would have been much more significant players in the container market world than they are today.

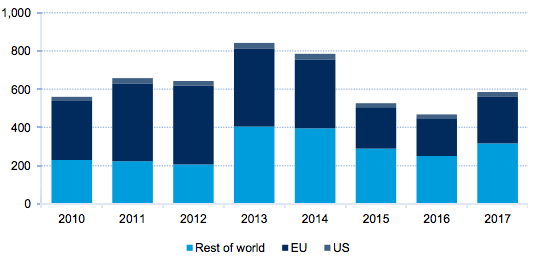

According to Drewry calculations, in that theoretical scenario Iran’s port handling last year would have been three time larger than it actually was, while Russia’s would have multiplied by 1.6, which collectively would have added an additional 8.7 million TEU to the world sum (see Figure 3).

Previous trading restrictions have meant that neither Russia nor Iran has lived up to its billing on the container market. A return to the trade wilderness through greater sanctions (deserved or not) will only increase the likelihood of that untapped container potential going to waste.